Monetisation Momentum : InvITs take centre stage while TOT faces uncertainty

08 December 2025

One such initiative aimed at creating an alternative funding source beyond traditional budgetary resources is the National Monetisation Pipeline (NMP). Under the NMP, new models such as infrastructure investment trusts (InvITs) have successfully channelled long-term capital, particularly from pension and insurance funds, into infrastructure projects.

Progress so far

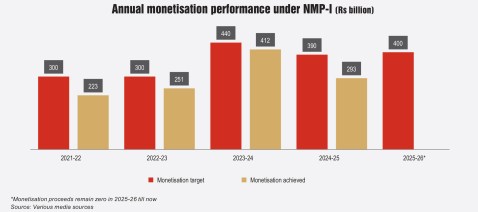

Under the first phase of NMP (NMP-I) announced in Union Budget 2021-22, the road sector was assigned a monetisation target of Rs 1.6 trillion for a four-year period from 2021-22 to 2024-25, accounting for over 26 per cent of the total target. In line with industry expectations, the sector emerged as a front runner in asset monetisation. By the end of the programme in March 2025, it had achieved approximately 73 per cent of its assigned target, raising over Rs 1.15 trillion and making a significant contribution to the overall monetisation effort.

At present, asset monetisation in the road sector is being undertaken through three routes – toll-operate-transfer (TOT), InvITs and toll securitisation. All three models have demonstrated different levels of success.

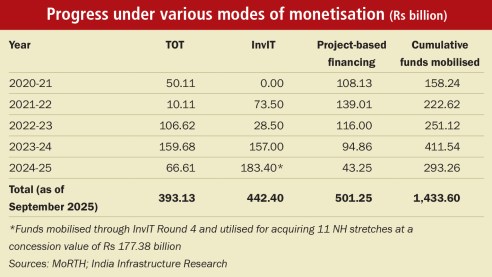

Policy evolution has shaped the sector’s funding mix, resulting in varied performance across models. The TOT model demonstrated fluctuating performance, peaking at Rs 159.68 billion in 2023-24. Meanwhile, InvITs, introduced after TOT, scaled up rapidly, reaching their highest annual contribution of Rs 183.4 billion in 2024-25. Project-based financing recorded the largest single-year contribution of Rs 108.13 billion in 2020-21, before slowing down, yet it remains the largest overall contributor in cumulative terms. The overall trend suggests a maturing asset monetisation market, marked by a strategic shift towards InvITs to attract stable, long-term capital.

Current market structure and trends

So far, the sector’s strong monetisation performance has set the stage for more ambitious targets. Under Phase II, the target has more than doubled to Rs 3.5 trillion. Moreover, the National Highways Authority of India’s (NHAI) recent report outlining strategies for more effective monetisation highlights the government’s focus on unlocking greater value from operational assets. However, questions remain about the preferred route, following the Ministry of Road, Transport and Highways’ (MoRTH) announcement of plans to phase out TOT in favour of InvITs. Achieving the targets discussed above will require a transparent and well-coordinated execution strategy, along with recognition that all monetisation routes are complementary rather than competing.

MoRTH’s decision to phase out the TOT model and increase reliance on InvITs stands in contrast to NHAI’s road map to offer three TOT bundles each quarter. This has created uncertainty regarding the future of the TOT model. Nevertheless, in July 2025, NHAI proceeded to invite bids for three new TOT bundles – 20, 21 and 22. These stretches recorded a cumulative electronic toll collection of around Rs 5 billion in 2024-25. Along with the previously invited bundles (TOT 15, 17, 18 and 19), NHAI is likely to raise Rs 210 billion-Rs 250 billion in 2025-26 from these seven TOT bundles. The authority is also yet to finalise concessionaires for Bundles 15 and 17, for which bids were received during 2024-25. With a bid value of Rs 92.7 billion, IRB Infrastructure Developers has emerged as the highest bidder for TOT 17. In addition, bids remain open for Bundles 18 and 19.

In addition, Macquarie has initiated plans to sell TOT Bundle 1, the first and highest-valued bundle awarded by NHAI to date. It is seeking an enterprise value of Rs 100 billion for a portfolio of nine road assets and is looking to sell these assets in three separate bundles. In another key development, Adani Road Transport has signed a share purchase agreement to acquire TOT 5 (A-2) from D.P. Jain for an enterprise value of up to Rs 13.42 billion.

On the InvIT front, NHAI has identified nine road stretches spanning over 550 km across Maharashtra, Odisha, Andhra Pradesh and West Bengal for monetisation in 2025-26 under the fifth round. The amount expected to be raised under this round will be half of what has been raised through InvITs in the past three financial years. In 2024-25, the National Highways Infra Trust acquired 821 km of highways from NHAI for an upfront payment of Rs 177.38 billion. This year’s target for fundraising through InvITs is Rs 150 billion, of which Rs 70 billion-Rs 80 billion will be raised through the fifth bidding round while the remaining contribution is expected from the public InvIT. Through the public InvIT, the government aims to give retail investors access to infrastructure assets that provide reliable returns over a long period of time. It will also help create a competitive environment in the InvIT market and mitigate the risks associated with a limited investor base.

The InvIT market has grown significantly in recent years, driven by policy reforms and regulatory support. Road InvITs have gained significant traction, accounting for nearly 50 per cent of total InvIT assets under management (AUM). In 2024 alone, these trusts accounted for over 50 per cent of the total asset deal value in the road sector, exceeding Rs 190 billion. Of late, private-listed road InvITs such as the Cube Highways Trust and Vertis Infrastructure Trust have expressed interest in going public. The Securities and Exchange Board of India has issued a consultation paper regarding easing the norms for this conversion. With a successful market debut, rising investor confidence and a steadily maturing market, industry experts estimate the road sector InvIT AUM to grow by 37 per cent, from Rs 2.4 trillion in March 2025 to Rs 3.27 trillion by March 2026.

Monetising future assets

With the closure of NMP Phase I, the government has launched NMP Phase II, significantly raising the monetisation target. Achieving the new target will require a substantial increase in the frequency and volume of InvIT issuances, especially if the TOT model is phased out. However, TOT bundles are not being discontinued completely – a strategic review is under way and policymakers may retain improved versions of the model to maintain a diversified investor base and address the potential risks associated with over-reliance on InvITs. If the monetisation target for the current fiscal year is achieved, collections of Rs 350 billion-Rs 400 billion would not only significantly exceed the Rs 243.99 billion raised in 2024-25 but would also surpass the monetisation target set for 2025-26.

While the government’s objective remains to maximise value for both investors and the public by unlocking the full potential of public assets, the choice of monetisation model will be critical. Moreover, although the sustainable roll-out of assets is a key priority for implementation, engaging with investors and learning from their viewpoints is even more critical.

With many assets in the pipeline, the road sector is brimming with opportunities. As per India Infrastructure Research, around 530 hybrid annuity model projects spanning more than 22,204 km are at various stages of implementation, presenting sizeable monetisation opportunities for investors. Looking ahead, the future trajectory is likely to bring further policy revisions, particularly in concession agreements and risk-sharing frameworks, to align with market realities and stakeholder expectations.